Clean Technology Investment Tax Credit (CT ITC) for Commercial Solar in Canada

A practical, plain-English guide for business owners, property managers, developers, and CFOs

If you’re exploring commercial solar (or solar + battery storage) in Canada, the Clean Technology Investment Tax Credit (CT ITC) can be one of the most important levers to improve your project economics—because it’s a refundable federal tax credit tied to the capital cost of eligible clean tech equipment.

At MAG Solar, we build commercial solar systems with incentive alignment in mind—meaning we help you understand what qualifies, what documentation typically matters, and how to structure a project timeline so it’s financeable and claim-ready (in partnership with your accountant or tax advisor).

This article is general information, not tax advice. Always confirm your strategy with your accountant/tax advisor and the CRA guidance for your specific situation.

But if you're thinking about making the switch, you likely have some important questions:

This comprehensive guide will answer all your questions and walk you through everything you need to know about the Clean Technology Investment Tax Credit (CT ITC)

🍁 Quick summary: what the CT ITC is (and why it’s a big deal)

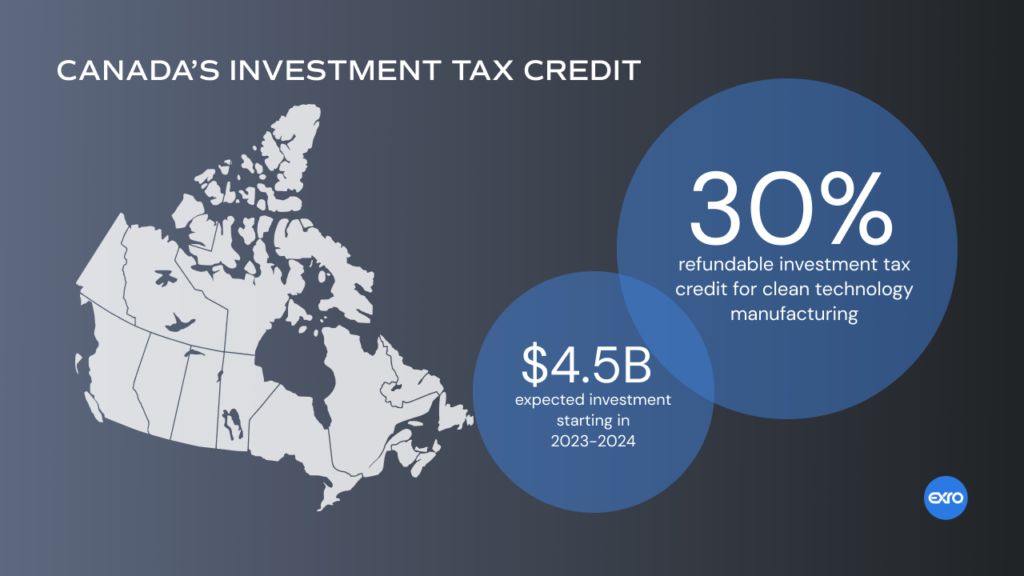

The Clean Technology Investment Tax Credit (CT ITC) is a refundable tax credit available for capital invested in new clean technology property in Canada during the program window.

- Program window: March 28, 2023 to December 31, 2034

- Credit rate:

- Up to 30% for eligible property that becomes available for use from March 28, 2023 to Dec 31, 2033

- Up to 15% for eligible property that becomes available for use in 2034

- Labour requirements can affect your rate: if you don’t elect to meet the labour requirements, the credit rate is generally reduced by 10 percentage points (example: 30% becomes 20%).

Why businesses care: the CT ITC can materially reduce net project cost and improve payback—especially for larger systems where the capital spend is significant.

Important note: This article is educational, not tax advice. Confirm eligibility and filing details with your accountant/tax advisor (and your legal counsel where appropriate).

Who can claim the CT ITC?

According to the CRA, to claim the CT ITC you generally must be:

- a taxable Canadian corporation (including one that is a member of a partnership), or

- a mutual fund trust that is a real estate investment trust (REIT) (including one that is a member of a partnership).

If your project is held inside a partnership structure, the CT ITC can be allocated to eligible members and reported through partnership slips (more on that below).

What commercial solar equipment can qualify?

The CRA lists categories of eligible clean technology property under the Clean Economy Investment Tax Credit (CT ITC). The categories most relevant to commercial solar projects include:

- Equipment used to generate electricity from solar (plus wind/water energy)

- Stationary electricity storage equipment that does not use fossil fuel in operation (example: batteries; also pumped hydro storage)

- Active solar heating equipment (and other listed heat technologies)

- Concentrated solar energy equipment

This is why Clean Economy Investment Tax Credit (CT ITC) discussions often include both:

- Commercial solar PV (your core generation asset), and

- Battery storage (where your business needs resilience, peak demand management, or operational stability).

The “must-haves” to qualify (the stuff people miss)

The CRA’s qualifying conditions include some deceptively simple requirements that can become very important during a review:

1) It must be in Canada and intended for use exclusively in Canada

The equipment must be situated in and intended for use exclusively in Canada.

2) It must be “new” (not previously used or acquired for use/lease)

Clean technology property generally must not have been previously used or acquired for use/lease for any purpose before acquisition by the taxpayer.

3) Leasing has extra rules

If the CT property is leased to another person/partnership, additional leasing requirements apply (including who it can be leased to and what business the lessor is in).

4) Timing matters: “available for use”

The credit rate depends on the date the property becomes available for use—and the CRA is explicit that eligibility hinges on that milestone.

How much is the Clean Economy Investment Tax Credit (CT ITC) worth?

(Simple math, real-world framing)

At a high level, the credit is calculated as a percentage of the capital cost of eligible clean technology property.

Here’s what that can look like in plain numbers (illustrative examples only):

Example A: $500,000 commercial solar project

Assume the eligible portion of capital cost is $500,000 and the system becomes available for use before the end of 2033.

- At 30%: potential credit = $150,000

- At 20% (reduced rate): potential credit = $100,000

That 10-point difference can be meaningful—especially if you’re sizing a system to hit an ROI threshold or financing requirement.

Example B: $1,200,000 solar + storage project

If your project includes solar PV plus battery storage (and those components qualify), the eligible base can be larger, which makes the credit larger too.

- At 30%: potential credit = $360,000

- At 20%: potential credit = $240,000

Again, the difference isn’t theoretical—it can impact loan sizing, DSCR, and approval timelines.

Labour requirements (why they matter, and how to treat them like a checklist)

The CRA’s Clean Economy Investment Tax Credit (CT ITC) rules include labour requirements tied to prevailing wages and apprenticeship participation. To benefit from the regular credit rate, you generally must elect to meet these requirements (and keep records to prove you complied).

When do the labour requirements apply?

The CRA states labour requirements apply when preparation/installation of the specified property is undertaken on or after November 28, 2023.

The two core labour rules

The CRA describes two main components:

- Prevailing wage requirements

Covered workers at a designated work site must be paid in accordance with the applicable eligible collective agreement (or equivalent wage + benefits logic if no agreement applies). - Apprenticeship requirements

Generally, you meet this by making reasonable efforts to ensure apprentices registered in a Red Seal trade perform at least 10% of total Red Seal hours at the designated work site during the year (for preparation/installation work).

“Elect + attest” (don’t skip this)

Where labour requirements apply, the CRA notes you generally need to:

- elect to meet prevailing wage + apprenticeship requirements for each installation tax year, and

- attest that you met them for each installation tax year and designated work site.

What happens if you don’t elect?

If you do not elect to meet the labour requirements, the CT ITC rate is reduced by 10 percentage points (30% becomes 20%; 15% becomes 5%).

Practical takeaway: treat labour compliance as a project deliverable, not an afterthought. In real life, it means contract language, reporting expectations, and record-keeping from day one—not “we’ll sort that out later.”

Can you combine CT ITC with other incentives?

Often, yes—but you need to be careful about what you’re combining and on which property.

You can’t double-dip on the same property across Clean Economy ITCs

The CRA notes you generally can claim only one Clean Economy ITC for the same eligible property (example: you can’t claim CT ITC if you claim the CCUS ITC on the particular property).

You may claim multiple ITCs in a project if you have different eligible property types

The CRA also notes that a project can include different eligible property types and may allow multiple ITCs for the same project (on different property types).

How CT ITC relates to accelerated depreciation (CCA / Class 43.1 & 43.2)

The CRA explicitly notes that additional tax incentives may be available for clean technology property also described in Class 43.1 and 43.2, such as accelerated capital cost allowance.

Translation: CT ITC is not the only lever—but it’s often the one that moves the needle most visibly, because it’s a refundable credit tied to capex.

🍁 Step-by-step: the CT ITC playbook for commercial solar projects

Below is a practical “project manager meets CFO” workflow you can use to keep your project incentive-aligned.

Step 1: Confirm your entity structure and eligibility

Before you price equipment or sign procurement:

- Are you a taxable Canadian corporation (or eligible REIT structure)?

- Will this be held in a partnership? If yes, plan for allocation/reporting pathways.

Step 2: Define what’s being installed and what likely qualifies

A clean bill-of-materials matters. You want to be able to identify:

- solar generation equipment,

- stationary storage equipment (if included),

- and any other qualifying clean technology property categories.

At MAG Solar, this is where we help you translate a design into a documentation-ready equipment scope.

Step 3: Build the “available for use” timeline (this drives your credit year and rate)

This is the timeline people underestimate. The CT ITC is tied to when eligible property becomes available for use.

So you’ll want to map:

- procurement lead times,

- construction windows,

- inspection and commissioning,

- interconnection approvals,

- and internal “in-service” documentation.

Step 4: Decide early: elect into labour requirements or accept reduced rate

If labour requirements apply (work on/after Nov 28, 2023), you generally choose between:

- electing + documenting compliance to access the regular rate, or

- taking the reduced rate.

This decision affects:

- contract terms,

- contractor reporting,

- apprentice scheduling,

- and record storage.

Step 5: Keep your documentation tight (so your claim survives scrutiny)

The CRA expects claimants to file complete, accurate, evidence-supported claims and keep records for labour requirements where applicable.

A good file usually includes:

- equipment invoices and proof of payment,

- commissioning documentation,

- as-built drawings / single-line diagrams,

- and (if electing labour) wage/apprentice records and related attestations.

Step 6: File correctly (this is where most “weird errors” happen)

The CRA outlines the claim pathway depending on entity type:

Corporations must generally include:

- Schedule 75 (T2SCH75) with calculation details, and

- Schedule 31 (T2SCH31) where the CT ITC claim is at line 155, included in totals on the T2 return.

Partnerships:

- complete Schedule 75 (T5013SCH75) and provide allocated amounts to members, with specific reporting boxes noted by CRA.

Eligible trusts (MFT-REITs):

- complete Form T1098 and claim on the T3 return as described by CRA.

Due dates + late filing:

You must generally file by the due date of your T2 (or T3). The CRA notes it may accept late filing of the appropriate information if filed no later than one year after the filing due date.

Recapture: the “10-year rule” you must understand

Recapture is the part many people skip until it bites them.

The CRA states that an amount of the credit may have to be recaptured in a taxation year for clean technology property acquired in the year or any of the preceding 10 calendar years if the property is:

- converted to a non-clean-technology use,

- exported from Canada, or

- disposed of.

The recapture calculation is proportional and will not exceed the CT ITC amount associated with the particular property.

Practical takeaway: if you might sell the building, change the use, restructure ownership, or remove equipment—tell your accountant early so they can model recapture risk.

Common CT ITC pitfalls (and how to avoid them)

- Assuming “it’s solar, so it qualifies”

Eligibility is category-based and rules-based. Confirm your equipment scope aligns with CRA categories. - Ignoring “available for use” timing

That milestone affects the year and rate. - Not deciding early on labour compliance

If labour applies and you don’t elect (or can’t document compliance), the rate reduction can be large. - Weak documentation from contractors

If you’re electing into labour requirements, the CRA places responsibility on the claimant and expects record keeping. - Not understanding recapture

The 10-year window matters for property changes, disposals, or exports.

How MAG Solar helps (without replacing your accountant)

Incentives don’t replace engineering—and engineering doesn’t replace tax advice. The best outcomes happen when they work together.

MAG Solar can support the project with:

- feasibility and preliminary design that matches the site and the business case,

- realistic production and offset modelling,

- equipment scoping and documentation that’s easy to hand to your tax team,

- construction planning that supports “available for use” timing, and

- coordination with your accountant/tax advisor so the technical plan and the filing plan match.

📞 Ready to Take Advantage of Commercial Solar Incentives in Canada?

If you’re considering commercial solar (or solar + storage) and want to understand how the Clean Technology Investment Tax Credit (CT ITC) could apply to your project, MAG Solar can put together a straightforward assessment with real numbers. Reach out for a free commercial consultation and we’ll review your site, your load profile, and the best-fit system approach—then help you prepare the project details your accountant will want for CT ITC planning.

At Mag Solar, we specialize in helping Canadian businesses navigate and maximize these incentives—from consultation to installation and everything in between.

✅ Book your FREE solar consultation today!

Let our experts:

Assess your commercial property

Identify which commercial solar incentives in Canada you qualify for

Provide a custom solar design and financial analysis

Help you claim your rebates and tax credits

👉 Contact Mag Solar now to start your solar journey with confidence.

📩 Email us at info@magsolar.ca

📞 Or call us directly at (604) 723-1222

Let’s power your business with clean, cost-effective energy—backed by Canada’s best commercial solar incentives.

- Let's Connect

Get a Free Commercial Solar Assessment

See How Much you Can Save with Solar. Get your Free Design & Consultation

It’s a refundable federal tax credit for capital invested in eligible new clean technology property in Canada, available within the program window described by the CRA.

It can be up to 30% for eligible property available for use through 2033 (and up to 15% for 2034), with reduced rates possible depending on labour elections.

Stationary electricity storage equipment (such as batteries) can qualify if it does not use fossil fuel in operation, per CRA categories.

The CRA indicates it’s claimable by taxable Canadian corporations and certain REIT structures (including when held through partnerships, subject to rules). capital cost deductions.

The CRA ties eligibility and rates to when the property becomes available for use, which is why commissioning and in-service timing matters.

The CT ITC is one of the key commercial solar incentives in Canada, offering a refundable tax credit of up to 30% for eligible solar projects. This applies to solar panels, energy storage systems, and other clean technology assets used in commercial or industrial operations across Canada.

Where labour requirements apply, claimants must elect to meet prevailing wage and apprenticeship requirements to access the regular rate, or accept a reduced rate.

The CRA states the labour requirements apply to work performed on or after November 28, 2023, when preparation or installation is undertaken on or after that date.

The CRA describes filing Schedule 75 (T2SCH75) and reporting the claim via Schedule 31 (T2SCH31) (line 155), included in the T2 total.

Yes — this is called a recapture. If you:

-

Sell the solar equipment

-

Export it outside Canada

-

Convert it for non-clean tech use

…within 10 years of claiming the credit, you may need to repay all or part of the CT ITC.

The CRA explains you may need to repay (recapture) some of the credit within the next 10 calendar years if the property is disposed of, exported, or converted to non-clean-tech use.